| | | | |

Answer: This is a question asked more than any other. Everyone

wants a definitive answer to it. Of course, anyone that claims they

can predict future interest rates is somewhat foolish or is making it up. I

am neither ... so the answer to this question is - it depends. It

depends on YOUR outlook for the future.

This page is becoming very long, almost a book! To make it easier for you to follow, I've broken it down into sections, showing my predictions and thoughts at various times in the past decade. Of course you should probably read the whole page from top to bottom to see my train and thought and to give you synopsis of what has happened with mortgage interest rates in the past, but you may just wish to navigate to the most recent post. I would recommend you read this entire page, it will allow you to follow my train of thought and thinking from start to finish.

2004 my thoughts and advice | 2007 update | 2009 update | 2011 update | 2012 Update | 2015 Update!

Are you an optimistic person?:

If you see a generally low inflation environment in the months ahead then you should stay as short of a term as you can, or lock in at the lowest variable rate in the marketplace, you could obtain a current variable rate mortgage at prime minus .7% or .9% You would save a great deal on interest and the odds are with you (If you locked in for five year closed mortgage, at say 2.50%, the prime rate would have to rise to over 4.00% from the current 2.7% that you can obtain on a 5 year variable rate mortgage before you were to pay the same interest as a five year rate. This could be a giant amount of monetary savings to you over the long term.

Are you a pessimist?:

If you believe inflation will be back and rates will generally rise over the next few years, then you may want to lock in your mortgage for 3 to 5 years. This will ensure stability of payments and fix your payments for many years. You could lock in for 5, 7 or even 10 years if you wish to be really secure with your payments. Today’s "typical" 10 year rate at about 6.1% (6.1 is the posted rate, 3.99% is the special rate you can obtain for a 10 year mortgage. - 25 year rate at 8.75% - and you can get out after 5 years (by law) with only a 3 months penalty. If rates go much higher (in an inflationary environment) or back to previous highs, the long term at this low rate will make your home attractive to future buyers.

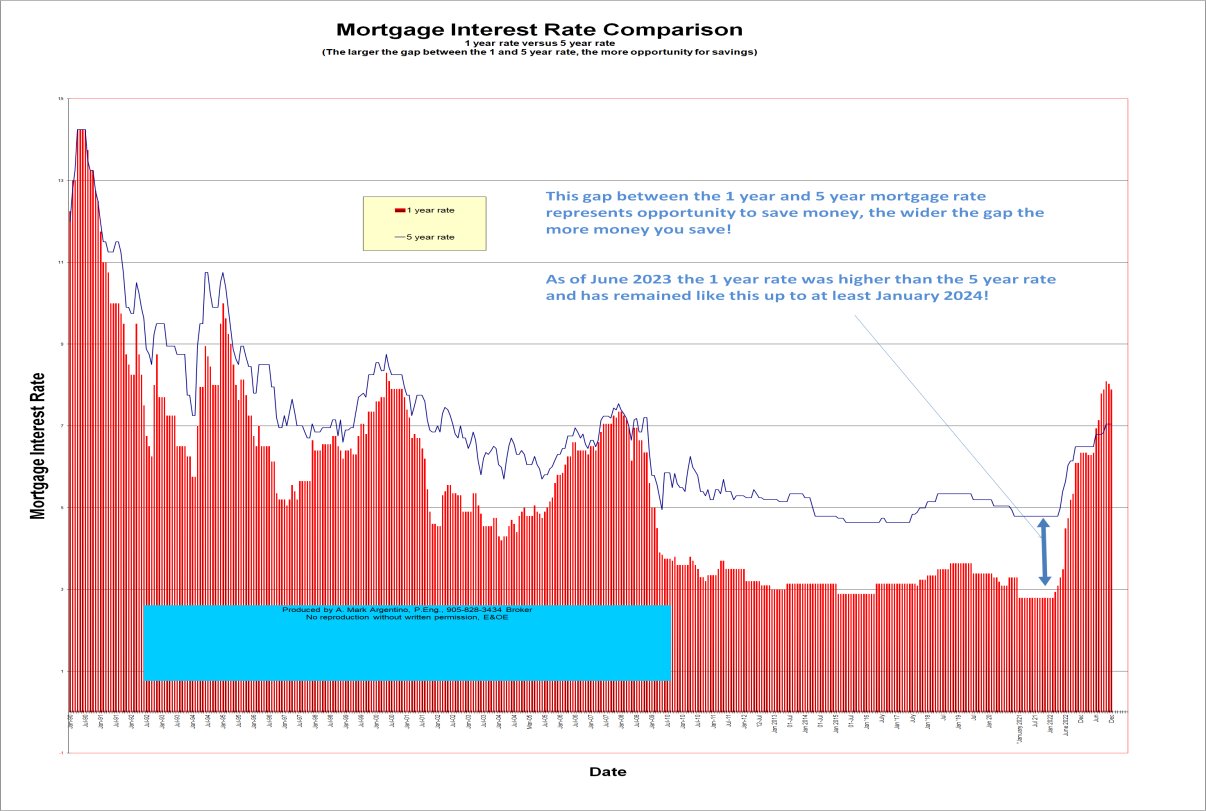

If you are not sure whether inflation or deflation is coming in the months and years ahead, then you may wish to play it safe by getting a variable open mortgage offering you the maximum flexibility ... or analyze the current market product where you pay ¼% over prime with the maximum interest is capped at 3.25% or so for 5 years. Other banks offer some such product as well, such as the BOM which offers a 2.65% variable rate capped at 4.15% for 5 years. There is also a product for the long term/short term mortgage from Scotia bank. | RBC advice | There are many options from all the major lenders.You may see a graph showing the spread between short

and long term mortgage interest rates and you will see that the wider

the gap the greater the savings in choosing a short term mortgage!

Whatever you decide to do, compare different lenders and options point by point and research the market in great detail before signing anything.

Are you a risk-avoider?... then you may wish to get a fixed rate long-term mortgage, or hedge your bets with a protected Variable Rate Mortgage.

If you're a risk-taker, simply stay with a short-term mortgage and watch closely for the signal to lock in a longer term deal. Wherever you can stand the additional cash flow requirement, increase your payment frequency and amount, and prepay principal wherever possible.

My personal experience is this.Written August of 2004 I bought my first property in 1984, a townhome at 2145 Sherobee Road in Mississauga and began paying a 25 year mortgage. Back then I had a low risk tolerance for changes in interest rates, so I initially locked in my mortgage for 5 years. In 1987, I moved to Calgary and broke my mortgage early, paid the 3 month interest penalty and renewed again at a 'better rate' In 1988 when I decided marketing and sales was the way to go in life and I changed careers, moved back to Mississauga and entered real estate sales. Again , I locked in for 5 years. Again, I had low risk tolerance and being self-employed I wanted some 'security' in my mortgage payments. In 1992 I locked in again for 3 years. Up to this point in my life, I had been making a huge mistake with my mortgage rate strategy and didn't even know it! In 1995 I finally 'saw the light' and decided to go short term on our mortgage. I increased my payment frequency to accelerated bi-weekly and reduced the amortization to 15 years. This saved me tens of thousands of dollars over a period of about 7 years. In hindsight, I should have gone with a short term mortgage from the very beginning in 1984. I performed some approximate calculations, but if I had decided to go with the short term mortgage rates from the very beginning in 1984, my savings in interest payments, charges for IRD (Interest Rate Differential) for my early mortgage renewals to gain a better rate (don't forget, mortgage rates in the mid to late 80's averaged about 12% !) and penalties for 'breaking' my mortgage when we moved to Calgary, would have been about $45,000! Yes, that's forty five thousand dollars more money that I just 'wasted' and would now have had in my pocket. Another way of saying this is that I could have reduced the amortization of my mortgage by about 3 years! If you look at the graph of short versus long term mortgage rates, you will see what I am referring to. Unless the gap between the long and short term rate is very narrow, it makes total sense to go short term. Even when the gap is small - it will widen again at some point - as the banks have to make money. The short term mortgage interest rates would almost have to double before you are breaking even and go up by about 150% for a few years before you were losing money by choosing short term. Another 'gem' of advice is this: go with accelerated bi-weekly payments and reduce your initial amortization from 25 years to about 22 or 20 or 18 years right from the very beginning, if you can tolerate the higher payments. The accelerated bi-weekly payments are a must. You will hardly notice any difference in your mortgage payments and in reality this strategy forces you to you make a full extra mortgage payment per year. This really adds up over time. Please follow this strategy as much as you can, you will thank me for dong this in 10 years from now. (Do your own calculations at my mortgage calculator page to see the difference, you'll be amazed at how much money you can save!) Another trick you can try. I know that all of this does not seem like much and it seems so far in the future, but, if you were to buy your first property and initially start with, say, a 21 year amortization for your mortgage (rather than the standard 25 years mortgage that most lenders want you to go with), in five years you have only 16 years remaining. Upon renewal, you pay off a little on the principal and then in another five years you would be down to 11 years remaining. (The math is not that difficult!). By this renewal time your income should have about doubled (compared to your income 10 years ago) and you should be able to comfortably increase your payments substantially and reduce your amortization to say eight years. Thus within 5 years you should be able to save up enough money to pay off the mortgage within another year or so. This means that rather than taking 25 years to pay off your mortgage, you will pay it off in 17 years or less. That's a huge difference, imagine having your mortgage paid off when you are 40 rather than 50! Read more about mortgage term, mortgage amortization and your interest rate. Bottom Line: Thus, your '25 year' mortgage just became 17 years, you saved a huge amount of interest and you are now mortgage free! Imagine the freedom. Even if you follow a plan that is remotely close to our experience, you will be far better off from a financial standpoint. You will have peace of mind and will have the freedom when you are 40 to 45 years old to do some of the things that you always wanted to do in life! I wish you and your family all the best! Mark

|

Update on Wednesday December 23, 2009 I wrote my experiences in the above text box almost two years ago. Since writing my last entry mortgage rates have been at all time lows. The Bank Prime interest rate has hovered at about 2.25% for most of this year and mortgage interest rates have only been about 1 to 2% above that. The Bank of Canada has "nearly promised" that they will be increasing the interest rates in the middle of 2010 (personally, I don't believe it, I think rates will stay low for another 10 years) Read about it here: read about interest rates at my blog and more here: If there is near certainty that prime rates may increase at least .25% to 1% or more by the end of 2010, then this may be the time for you to think about locking in your mortgage for a longer term. (Even though I don't recommend doing this, unless you have very low interest rate increase tolerance). The logic is that we may never see these historic low interest rates for at least the next 10 or 20 years or even longer. If this is the case and prime rates increase by 1% or more from now to the end of 2010, then it may be time for you to lock in your mortgage for a longer term. (Again, only if you have low tolerance rate increase, otherwise stay with variable to save money) This short analysis below will give you something to think about. I will use the Royal Bank current posted mortgage rates as an example of rates. See them here Current short term open variable rate mortgages are prime plus .7% for the open variable rate mortgage and prime rate for 5 year closed variable rate mortgage. Thus, if you have an open variable rate mortgage and the bank prime increases 1% by the end of 2010 then your mortgage rate would increase from the current 2.95% to 3.95% If you have the closed variable rate mortgage it would increase from 2.25 to 3.25% Current closed 1 year mortgage rates are 3.40% and 5 year closed mortgage rate is 5.49% If the bank prime increases 1% by the end of 2010 it is not a certainty that the 1 and/or 3 year rates will increase by 1%. It's possible they will increase more than 1% if the longer term estimates at the end of next year are that rates will continue to increase. If the longer term estimates at the end of next year are that rates will stay about the same or possible decrease in the first half of 2011 then longer term rates will likely not increase by as much as 1%. This is because less people will want to lock into longer term mortgages if the future rates are predicted to drop and the banks will offer good rates for people who lock into longer mortgages if this is the case. Another complicating and very compelling reason to lock into longer term mortgages before the prime rate increases in the middle of 2010 is that RBC and other banks are predicting that the Bank of Canada Prime Rate is expected to increase from the all time low of .25% today to nearly 3% by the end of 2011. See this prediction graph If this occurs, as the RBC is guessing and predicting that it will, then mortgage interest rates will increase to about 2.5 to 3% ABOVE what they are today. Thus a short term variable rate mortgage may increase to about 6% or so. The one year rate would increase to about 6.5% and 5 year mortgages to 8.49% If you can obtain a 5 year mortgage today at 5.49% versus 8.49 in 2 years, then locking in now or soon may be the route to go. But, notice that current short term variable is at 6% in this example and 5 year long term mortgages are 5.49% if you were to lock in today. So again, the philosophy that I have subscribed to for many years is still almost about the same. Short term mortgages are about the same as longer term mortgages even when the prime rate increases 2.75% This also means that bank prime would have to increase by more than 3% for you to be in a negative position compared to if you decide to continue with short term mortgage rates. Another factor to consider is that banks will often offer 'specials' on their rates and although posted rates may be high, these rate specials may make it very attractive to lock into a long term mortgage or even a prime minus a large percentage on a 5 year variable rate mortgage. So, what's the bottom line? Once again, the decision to go short or long term on your mortgage rests with your risk tolerance and your ability to make the payments depending upon your personal situation. I wish you all the best in 2010 and beyond! Mark |

|

My how time flies! Had you followed my recommendation made back in 2009 for choosing variable rate on your mortgage, you would be saving a fortune in interest on your mortgage by now! :-) I've added a proviso on that statement I made back in 2009, you would only lock in if you have low tolerance for rate increase. The reason for me to make this statement was because most banks were predicting that the prime rate was about to jump from .25% to 3% or more, even the Royal Bank was saying this, See RBC Prime Rate prediction graph here Thus, if the bank prime had increased to 3% then mortgage rates would now be about 6 to 8% and locking in back in 2009 would have been wise, but ONLY for people with low interest rate tolerance. Again, the major stipulation about locking in back in 2009 was if the prime rose from what was then at .25% to 3%, as many banks were predicting, the Royal Bank being one of them. Since the prime is still at 1% and may go to 1.25% or even 1.5% by the end of this 2011, you are still far ahead of the mortgage game choosing variable rate. I would only recommend locking in your mortgage if you have a low tolerance for rate increases or some other unusual circumstances. Otherwise, I firmly believe that variable rate mortgage is the best method to save yourself money. Variable is exceptionally attractive right now, April 2011, because most lenders are offering prime minus .7% to prime minus .9% and this is a huge break that you can take advantage of for the next 5 years. Even if prime doubles to 2% or even triples to 3% then bank prime would likely rise to 4% or 5% but you are still far ahead over the next 5 years by staying with the variable rate due to your mortgage being prime minus .7% or .9%. If you want interest rate security, then you go long term. If you want to save money, my advice is to go variable, always (at least for the next 2 to 4 years). ....and this is why

I wish you and your family all the best in 2011! Mark PS: No sooner had I posted the above update, I read an article in the Globe and Mail that states that the Bank of Canada announced that an interest rate increase is almost a certainty and some are predicting a 0.5% increase! Read the article here! |

|

This is a running record of how interest rates have changed over the past 5 to 10 years and what my personal philosophy is regarding what you should do with your mortgage - namely, should you lock in your mortgage interest rate or should you stay with a variable rate mortgage. This is the question! Currently, the bank prime is 3% and mortgage rates for fixed term are nearly the same. There are 4 year mortgages at 2.99% almost everywhere. You can get a 5 year rate at 3.5% These are 50 year historic lows- meaning, it could be time to lock in your rate if you are not a gambler. We have seen a price war for 4 year mortgage interest rates for the past couple of weeks. BMO was one of the first out of the gate to offer 2.99% for a 4 year mortgage, the other banks and lenders followed shortly thereafter. Now you can see 5 and 10 year mortgage interest rates at absurdly low levels. I've seen 5 year fixed rate mortgages at 3.5% which is unbelievably low. Don't forget these are posted rates and often you can get a lower rate than posted if you negotiate. Variable rates - the banks are posting their rates as prime plus .1% and you can find prime minus .2% Fixed rate mortgages are very attractive right now. If the longer term rates do increase next year then the variable rate discounts could be larger than what they are now and if you can lock in a variable rate in 2 years from now, you may still do very well compared to longer term rates. But, the current 4, 5 and 7 year rates are very tempting to lock into. I've written many articles about staying with short term mortgage rates at this page: lock in short or long term My preference for many years has been to go variable, but if you are not a gambler, then it could be getting close to the time where you lock in your mortgage. Read the article below that just appeared in the POST, it's very interesting what the experts are saying. If you want interest rate security, then you go long term. If you want to save money, my advice is to go variable, always (at least for the next 1 to 1.5 years). ....and this is still why Stay Tuned....... All the best! Mark |

|

It's been almost 3 years since I wrote to you on this page! This page is a running record of how interest rates have changed over the past 5 to 10 years and what my personal philosophy is regarding what you should do with your mortgage - namely, should you lock in your mortgage interest rate or should you stay with a variable rate mortgage. This is the question! After nearly 4.5 years, the Bank of Canada made an announcement last week that shocked the experts, they lowered the Prime Rate by 0.25% Nobody was expecting this reduction! The reasons behind the drop are varied, but the largest reason is that the price of oil is under $50 per barrel and the Bank of Canada performs most of it's forecasting based upon the assumed price at $60 per barrel. Thus, with low inflation, low oil prices generating lower overall revenue for Canada (and certainly Western Canada) the bank decided to lower the rate. Read about the current Bank of Canada Prime Rate Update The major Canadian banks did not immediately lower their prime rates that they charge their best customers. As a matter of fact, the Banks only lowered their prime rate by .15% and not the .25% that the Bank of Canada dropped the rate. Bank prime is now 2.85% and mortgage rates for fixed term are nearly the same. Many believe that there will be mortgage rate wars over the next few months. The banks still have plenty of cash to lend so this is likely the case. We are still at or near 50 year historic lows- meaning, it's still a good time to 'lock in' your rate if you are not a gambler. Again, please don't forget these are posted rates and often you can get a lower rate than posted if you negotiate. Variable rates - the banks are posting their rates as prime plus 0.000% and you can likely find prime minus .2% to prime minus .5% or possibly more I've written many articles about staying with short term or variable mortgage rates at this page: should you lock in short or long term My preference for many years (and continues to be) to go variable, but if you are not a gambler, then it could be getting close to the time where you lock in your mortgage. I recall reading an article the day of the rate cut on January 21, 2015 that not one of the 19 'experts' on the Bloomberg Panel had predicted a rate cut. Now if you read about predictions for the March 4, 2015 Bank of Canada Interest Rate Announcements the 'experts' are saying that they expect the bank rate to drop another .25% Read the article below that just appeared in the Herald about rates, it's very interesting what the experts are now saying about rates. If you want interest rate security, then you go long term. If you want to save money, my advice is to go variable, always (at least for the next 1 to 1.5 years). ....and this is still why

The mortgage interest rate debate continues..... All the best! Mark |

Remember ...because mortgage interest is not tax-deductible, every dollar you pay off your mortgage gives you an AFTER TAX RETURN of whatever your rate is, because you're saving interest you'd otherwise have to pay with after-tax dollars! This is assuming that you are not using the "Smith Manoeuvre" or something similar to make your principal residence mortgage tax deductible.... but that's another story!

I've decided that I will begin to dedicate this webpage to some of my past and current clients that I have connected with or that I feel could really benefit from this 'unsolicited' advice above. They know who they are and some of them I want to give an honourable mention to keep them motivated:

- Iain and Leaha (I wish all my clients were like you two were and wish you many years of success and happiness)

- Sonja and Mark (I wish all of my clients were as excited about buying a home as you were! You were a real pleasure to work with)

- John and Roodya (I wish all my clients gave me hugs and encouragement like you two did!)

- Fabio and Kelly (I wish you all the best of success and happiness and I hope you stick to your plan)

- Scot and Julia (One of the most enjoyable and fun sale of a house and purchase of a house)

- Marna and Isabel (I hope that this page inspires you to follow your own plan and enjoy your upcoming new life and baby! wish we could have spent more time together)

- Norm and Sue (You have everything under control and I never learned so much as I did from the two of you)

- Mike and Laurie, Steve and Linda, Silvyn, Joerg and Kathrin, Colin and Sharon, Gary M. (what a class guy), Dave and Lorna, Jim and Marcy, Tar and Suneeta, Deb S. just some of my past clients that I reflect upon with such happiness and satisfaction - none of you really know how much I appreciate your business and how happy I am that you were able to sell for top dollar and buy such a great home

- I've reached a point in my career (over 28 years) where I can look back at the 100's of families that I have helped and say that it really is truly satisfying to have helped all of you reach your goals, dreams and aspirations. I am blessed to have been able to work with such nice people as you.

I wish you all much success, good health and happiness - always,

Mark

Should you go with a short or long-term mortgage?

A longer-term mortgage is worth considering if you have a busy life and don't have time to watch mortgage rates. RBC's 4, 5 and 7-year mortgages let you take advantage of today's rates, while enjoying long-term security knowing the rate you sign up for is a sure thing.

Read more about the Royal Bank Advice on long or short term mortgage and what's best for you!

If you want to keep your mortgage flexible right now, you can explore a shorter-term

mortgage that usually allows you to take advantage of lower rates and save.

The long and short term mortgage from Scotiabank

What Type of Mortgage You Should Get If you are buying a home with less than 25% down payment your choices of mortgage products and terms are somewhat limited...3 year fixed rate or longer under the regular CMHC Program and 5 years fixed rate or longer under the 5% down program.

However, if you are not constrained by the insurance requirements of a high-ratio mortgage there are many options available...they are summarized below. (Note: Not all lenders offer all types of mortgages.)

CATEGORIES and types of mortgages

You may see a graph showing the spread between

short and long term rates and you will see that the wider

the gap the greater the savings in choosing a short term mortgage!

| |

Mississauga MLS Real Estate Properties & MLS.CA Homes for Sale | All Pages including Mississauga Real Estate Blog all maintained by info@mississauga4sale.com Copyright © A. Mark Argentino, P.Eng., Broker, RE/MAX Realty Specialists Inc., Brokerage, Mississauga, Ontario, Canada L5M 7A1 (905) 828-3434 First created - Tuesday, July 16th, 1996 at 3:48:41 PM - Last Update of this website: Tuesday, April 9, 2024 7:24 AM

At this Mississauga, (Erin Mills, Churchill Meadows, Sawmill Valley, Credit Mills and or Meadowvale ) Ontario, Canada Real Estate Homes and Property Internet web site you will find relevant information to help you and your family.

Why Subscribe? You will receive valuable Real Estate information on a monthly basis - such as: where to find the 'best' mortgage interest rates, Power of Sale Properties and graphs of current house price trends. Plus, you will pick up ideas, suggestions and excellent real estate advice when you sell or buy your next home.

Read Past Newsletters before you decide |