| | | | |

Choosing between a fixed or variable rate mortgage is not a simple decision,

which is why many people are looking for advice to help them decide which mortgage

interest type is best for them based on their personal circumstances.

You can choose to go with a stable, fixed rate mortgage. Or, you may feel more comfortable with the risks and potential rewards of a variable rate mortgage.

For the "best of both worlds," you might decide on a mortgage that combines both interest types. It really depends on your tolerance for risk, as well as your current goals and the life stage you are in.

Here is some information about each option to help you make the right choice.

Fixed rate mortgages are chosen because of the high level of stability they provide.

A fixed rate mortgage offers the security of locking in your interest rate

for the term of your mortgage. This means you'll know exactly how much principal and interest you will be paying on each regular mortgage payment throughout the term you select.

The main advantage of selecting a mortgage with a fixed interest rate is that

you can depend on an interest rate that stays the same during the term of the

mortgage. The down side is that you can't take advantage of a lower interest rate — and the ability to have more of your payment go towards the principal and less to interest — if interest rates drop during the term of your mortgage.

|

|

The case for variable ratesMany Canadians shy away from the option of a variable rate mortgage because of the potential risk of rate increases. However, while there is always a risk of interest rate fluctuations, this concern may be less of a factor than you may think, and there are other reasons to consider a variable rate mortgage. Many Canadian economic experts believe that a mortgage rate that varies with fluctuations in the bank's prime rate will offer the greatest advantage when it comes to long-term savings on interest costs. |

Examining Canadian mortgage rate data from 1950 – 2007, Dr. Moshe Milevsky, Associate Professor of Finance at York University, found:

The case for both fixed and variable rates in one mortgage Not sure about putting all your eggs in one basket? Now you don't have to.

If you have sufficient equity in your home, the RBC Homeline Plan® might be for you. It gives you the flexibility to choose both fixed and variable rate options, all in one plan.

You can split your mortgage between fixed and variable rates with different terms and maturities in order to benefit from potential interest savings and the security of a predictable rate. Whether rates remain stable or fluctuate, this strategy reduces the risk of making a bad decision and could save you thousands of dollars in interest costs over the life of your mortgage.

Which should you take?

Your RBC® mobile mortgage specialist can advise you on the current rates offered by RBC Royal Bank® and help you decide which mortgage option best fits your situation and risk tolerance.

To help you start thinking about what's

right for you, here are some general

guidelines to consider:

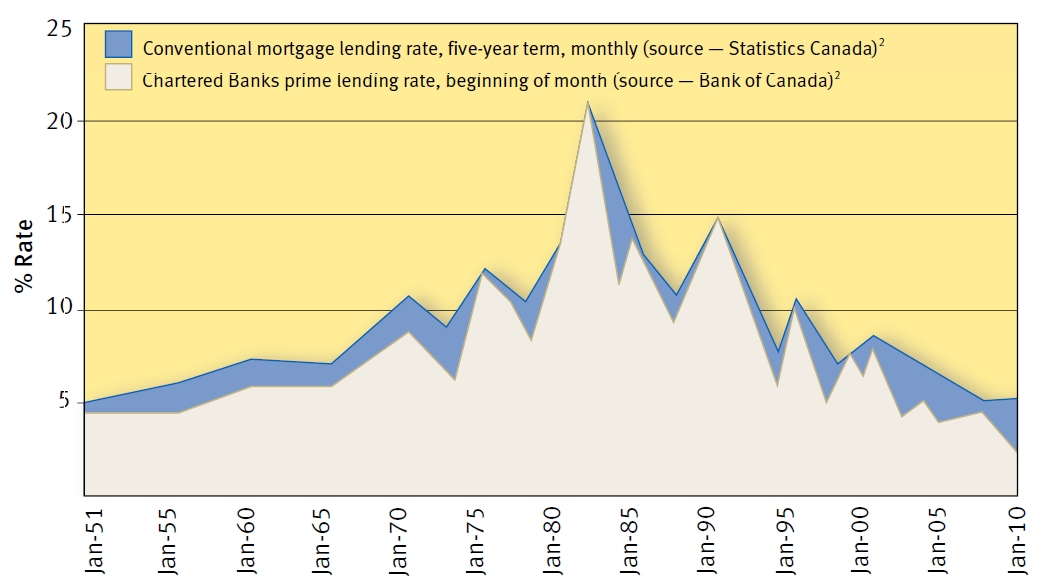

By taking a look at the chart above, you can see that except for a brief period of volatility between 1980 and 1984, the five-year rate stayed between 5% and 7% between 1951 and 2010. The chart shows how a fixed rate mortgage can have both a positive and negative impact over the long term. When rates moved up, those with a fixed rate were protected against fluctuations while when rates moved down those with fixed rates did not receive the benefit of lower interest rates. With a fixed rate mortgage, amortization remains constant despite rate fluctuations.

The primary concern clients have with variable rate mortgages is the risk of interest rate fluctuations in an environment of increasing rates. As you can see, since the early 1980's, there has been a declining trend in prime rates† overall, which has favoured clients who chose variable terms. However, the opposite was true through the 1970's and early 1980's when prime rates increased. Interest rates have been exceptionally low through 2009 and early 2010 and it is widely anticipated that they will start to increase in the second half of 2010.

This may favour locking in a fixed rate today over choosing a variable rate. Choosing both a fixed and variable rate

If you are unsure about your level of risk tolerance for rate fluctuations, choosing both allows you to take advantage of the lower interest rate of a variable rate mortgage and the security of a fixed rate mortgage.

The reality is no one can be certain what the future holds. Rather than trying to guess where rates are headed, it's best to consider your own situation.

The life stage you are in, your current goals, your objectives and your tolerance to risk all come into play.

Used with permission from Royal Bank Canada

You may see a graph showing the spread between short and long term mortgage interest rates and you will see that the wider the gap the greater the savings in choosing a short term mortgage!

Whatever you decide to do, compare different lenders and options point by point and research the market in great detail before signing anything.

Read about my observations and advice on locking in a variable rate mortgage or fixed rate

I wish you all much success, good health and happiness always,

Mark

You may see a graph showing the spread between

short and long term rates and you will see that the wider

the gap the greater the savings in choosing a short term mortgage!

| |

Mississauga MLS Real Estate Properties & MLS.CA Homes for Sale | All Pages including Mississauga Real Estate Blog all maintained by info@mississauga4sale.com Copyright © A. Mark Argentino, P.Eng., Broker, RE/MAX Realty Specialists Inc., Brokerage, Mississauga, Ontario, Canada L5M 7A1 (905) 828-3434 First created - Tuesday, July 16th, 1996 at 3:48:41 PM - Last Update of this website: Tuesday, April 9, 2024 7:24 AM

At this Mississauga, (Erin Mills, Churchill Meadows, Sawmill Valley, Credit Mills and or Meadowvale ) Ontario, Canada Real Estate Homes and Property Internet web site you will find relevant information to help you and your family.

Why Subscribe? You will receive valuable Real Estate information on a monthly basis - such as: where to find the 'best' mortgage interest rates, Power of Sale Properties and graphs of current house price trends. Plus, you will pick up ideas, suggestions and excellent real estate advice when you sell or buy your next home.

Read Past Newsletters before you decide |