How is the bank rate set in Canada and how does it affect the mortgage interest rates?

How the Bank of Canada Determines Its Target Overnight Rate. The Bank of Canada makes its decisions based on the growth of the Consumer Price Index (CPI) from Statistics Canada.

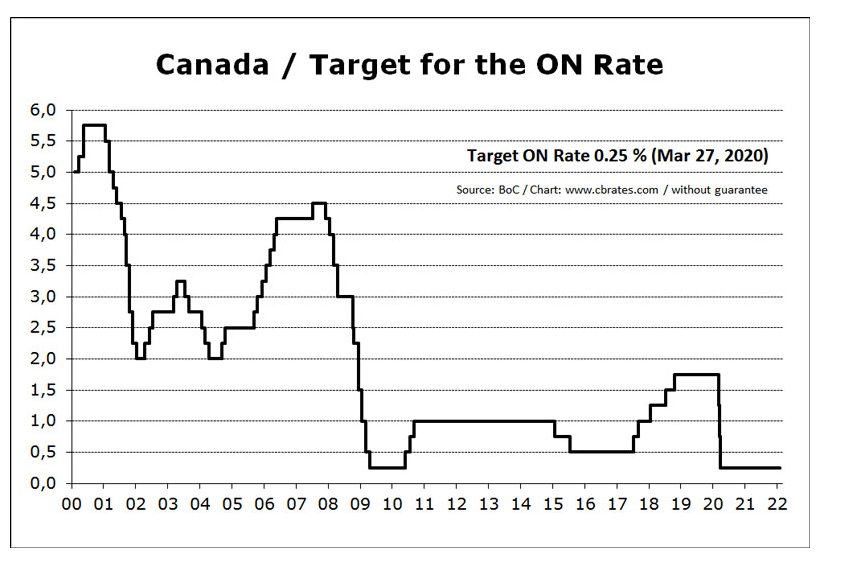

For more information on the policy interest rate, see this explainer.

At the heart of the Bank of Canada’s monetary policy is the target for the overnight rate. See what it is—and what it means for you.

The target for the overnight rate

At the Bank of Canada, the primary tool we use to control inflation is our target for the overnight rate—also called our policy interest rate. This is the starting point for setting many of the interest rates in the economy that matter for Canadians.

The overnight market

Every business day, Canada’s financial institutions move money back and forth among themselves for their customers. Whenever you use your debit card or send an e-transfer, money flows between financial institutions. At the end of each day, they need to settle all these payments. Some institutions may have sent out more in payments than they received, while others may have received more than they sent.

To get back to balance, financial institutions can borrow money from each other for one day in the overnight market. The Bank sets a target for the interest rate we want financial institutions to charge each other when they make these overnight loans.

Deposit rate and bank rate

Financial institutions don’t have to borrow from each other to get back to daily balance—they can also use the Bank. They can deposit money with us at the deposit rate for one night or borrow money from us at the bank rate for one night.

The range between the deposit rate and the bank rate—called our operating band—is usually one-half of a percentage point wide, with our policy interest rate sitting in the centre. For example, if the Bank sets the policy interest rate at 2.25 percent:

The lower end of the range is 2 percent—our deposit rate.

The higher end of the range is 2.5 percent—our bank rate.

How this actually works

In reality, financial institutions almost always choose to borrow and lend among themselves. This is because the whole system always balances. An institution that needs money knows there is another institution with extra money to lend.

The difference between the deposit rate and the bank rate encourages financial institutions to do this borrowing and lending with each other instead of coming to us. For example:

Bank A has extra money. It can earn more interest by lending that money to Bank B than by leaving it with us and earning the deposit rate.

At the same time, Bank B needs money. It would rather borrow at a lower rate than at our bank rate. So, it’s better for Bank B to borrow from Bank A.

This gives a powerful incentive for banks to borrow and lend within this band. When we adjust our policy interest rate, we also adjust the deposit rate and the bank rate by the same amount to maintain the operating band.

In response to the 2007–09 global financial crisis and again in 2020 during the COVID-19 pandemic, the Bank cut the policy interest rate to 0.25 percent to support the economy. With the rate at this level, the Bank temporarily set the deposit rate at the same level as the policy interest rate, resulting in an operating band of 0.25 percent to 0.50 percent.

What it all means for you

The public doesn’t access this overnight market to borrow or lend money. Still, our policy rate and this market are important to you. By encouraging financial institutions to borrow and lend among themselves at close to the policy rate, the Bank affects interest rates on all kinds of other borrowing in the economy, including:

the prime rate of commercial banks (used for loans such as lines of credit)

mortgage rates interest rates paid on deposits, guaranteed investment certificates and other savings

What’s behind your mortgage rate? Find out from The Economy, Plain and Simple.

Why we change the target

If the economy is struggling to grow, it could pull inflation significantly below 2 percent. In response, we might lower the policy rate so that other interest rates across the economy go down. This means:

People and businesses pay lower interest on loans and mortgages and earn less interest on savings.

With lower rates, people tend to spend more, boosting the economy.

But if the economy is growing too fast, it could lead to rising inflation. So, we might raise the policy rate, which means:

People and businesses pay higher interest on loans and mortgages. This discourages them from borrowing, reduces their spending and puts the brakes on inflation.

With higher rates, people tend to save more and spend less, slowing down the economy.

You may continue to read the information on this page, but it stops at

2006. Use this page for more current information on how the Bank

of Canada Sets the Rate.

The Bank of Canada today announced in early March of 2006 that

it is raising its target for the overnight rate by one-quarter of one

percentage point to 3 3/4 per cent. The operating band for the overnight

rate is correspondingly increased, and the Bank Rate is now 4 per cent

The Bank of Canada hiked its trend-setting Bank rate in December 2005 to 3.5 per cent. The Bank began raising it in the autumn of 2004, when it stood at 2.25 per cent.

The Bank has signaled its intention to continue hiking the Bank rate, which is widely expected to rise by a further one quarter of a percentage point between now and the late spring of 2006. The Canadian Real Estate Association expects the Bank rate to top out and stabilize at 3.75 per cent by mid-year.

The Bank is concerned about the potential for renewed inflation since. This has been the banks main concern over the past 5 years or so. There is ample evidence that there is virtually no slack in Canada's product and labour markets. Canadian economic growth is forecast to be 2.9 per cent in 2006, which slighter faster than its estimated non-inflationary rate of 2.8 per cent.

Financial markets think a rising Bank rate hike will keep inflation under wraps. Since bonds respond to inflation expectations and mortgage rates track bond yields, the five-year conventional mortgage rate is expected to rise by no more than one-half of a percentage point in 2006.

At the end of 2005, the five-year conventional mortgage rate stood at 6.3 per cent with this being the posted rate. Stiff competition among mortgage lenders continues to help borrowers negotiate discounts of about one per cent or even more off the advertised rate. Higher mortgage rates are expected to only gradually cool resale housing activity in 2006 and should have an effect on the Toronto Real Estate market prices.

No. The Bank of Canada sets the "target for the overnight rate." The overnight rate is the interest rate that banks charge each other to cover their short-term daily transactions. The target for the overnight rate is a half-percentage-point band.

If, for instance, that band is 3.25 per cent to 3.75 per cent, it means that banks will charge 3.75 per cent interest on money they lend to other banks and pay 3.25 per cent interest on money deposited by other banks. A nice setup!

The chartered banks use the overnight rate as a guide in setting their prime lending rate – the rate at which the bank's best customers can borrow money. When the central bank changes its overnight rate, it's sending a signal to the chartered banks that it wants them to change their prime lending rates. The banks always follow suit; if the central bank raises its overnight rate and a bank leaves its prime rate unchanged, it will make less profit.

The Bank of Canada does not directly set mortgage rates or credit card rates. Variable mortgage rates and other floating rate loans like lines of credit move up and down in lock step with the prime lending rate. But the rates for fixed mortgages depend more on the bond market.

Banks rely on the bond market to raise money for those kinds of mortgages. Interest rates on the bond market can move up or down more frequently than the prime rate because the bond market is far more sensitive to market fluctuations. Rates move when traders believe the central bank may be about to increase – or reduce – interest rates. You can find more about this and other Bank of Canada Monetary policies at Bank of Canada. This information is mostly from cbc.ca/news As of

March 5, 2022

the Bank

Prime Rate was 2.50%

Why Subscribe?You will receive valuable Real Estate information on a monthly basis - such as: where to find the 'best' mortgage interest rates, Power of Sale Properties and graphs of current house price trends. Plus, you will pick up ideas, suggestions and excellent real estate advice when you sell or buy your next home.

Read Past Newsletters before you decide Privacy-Policy

send me an email

with the MLS numbers and I'll get you the full MLS listing right away!

send me an email

with the MLS numbers and I'll get you the full MLS listing right away!